Here’s your wake-up call for 2026: a business that doesn’t accept online payments isn’t a modern business. Period. The evidence? In just ten years (2014-2024), the share of global online sales driven by digital payments doubled – from 34% to a dominant 66%. This isn’t some passing trend you can ignore. It’s the fundamental landscape of commerce now. Adapt or get left behind.

What Are Recurring Payments & How Do They Work?

Sell Without Borders

Close More Sales

Money Moves Faster

Meet Real Demand

Who Needs to Accept Online Payments?

A Home Decor Shop

A Financial Consultant

A Project Management SaaS

An Animal Shelter

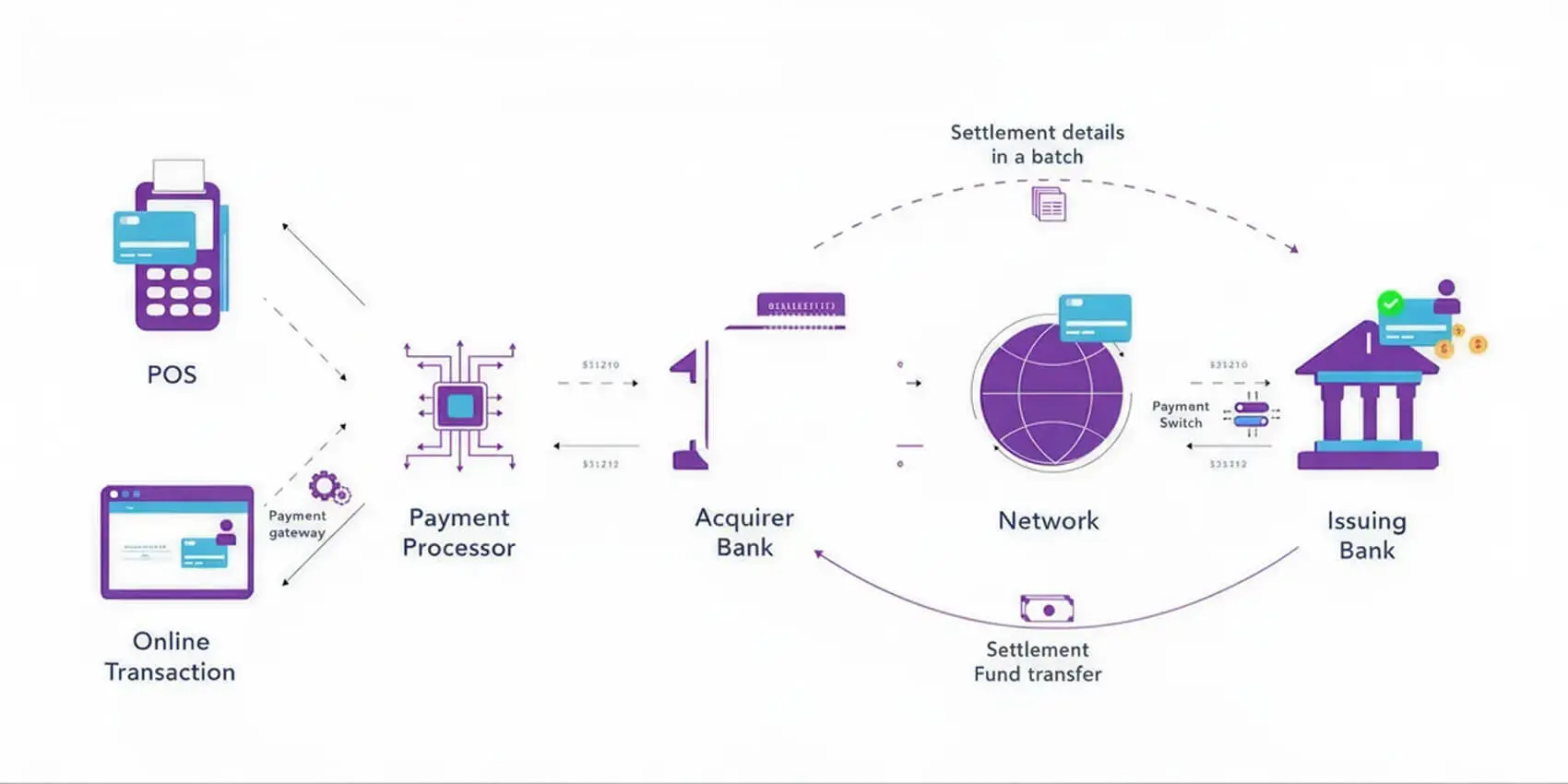

How Online Payments Work: The Technology Demystified

1. Initiation

2. Encryption & Routing

3. Authorization

4. Completion

5. Settlement & Funding

Popular Online Payment Methods to Accept in 2026

- Credit & Debit Cards: the most typical. Need to Have, though big on PCI DSS.

- The world’s leading online payment method is now digital wallets (such as Apple Pay, Google Pay, and PayPal), which will comprise 53% of the value of all e-commerce transactions in 2024. ProsThey provide better security with tokenization and a quicker one-tap checkout.

- Bank Transfers & ACH: good for B2B invoices, large transactions or recurring payments due to much lower fees.

- Buy Now, Pay Later (BNPL): afterpay and Klarna are no longer on the fringe. They can rise average order value by 20-30% and are a hit with the younger generations.

- Cryptocurrency: still in its infancy, but accepting crypto (through dedicated gateways) can appeal to a tech-savvy customer base and help in borderless transactions.

- Mobile & Contactless: Tap to Pay on Mobile technology transforms any modern smartphone into a mobile POS, which is a game-changer for service providers, delivery drivers and market vendors.

Choosing the Right Payment Gateway

| Factor | What to Look For | Why It Matters |

|---|---|---|

| Fees & Pricing | Transparent, interchange-plus pricing. Watch for hidden chargeback fees, monthly minimums, and setup costs. | Directly impacts your profitability. Predictable costs are vital for small businesses. |

| Security & Compliance | Built-in fraud protection tools (machine learning, 3D Secure 2.0) and full PCI DSS compliance support. | Protects your business and customer data. A breach can be catastrophic. |

| Integration & Developer Experience | Seamless eCommerce integration with your platform (Shopify, BigCommerce). A clear, well-documented API for custom builds. | Saves time and cost during setup and future scaling. |

| Supported Payment Methods | All major credit/debit cards, digital wallets, ACH, and relevant regional methods. | Meets customer expectations wherever they are. |

| User & Checkout Experience | Branded, mobile-optimized, and fast checkout pages. Low-friction flows. | A poor checkout experience is a primary cause of cart abandonment. |

| Customer Support & Uptime | 24/7 support via multiple channels and a guaranteed uptime of >99.9%. | When payments stop, your business stops. Reliable support is non-negotiable. |

Step-by-Step Guide: How to Accept Payments on Website

Analyze Your Business Needs

Obtain a Merchant Account

Select Your Payment Gateway

Integrate the Gateway

-

For E-commerce Platforms

Use a native plugin or extension (e.g., the "Square for WooCommerce" plugin).

-

For Custom Websites

To enable payment through website for custom builds. Utilize the provider's API for a fully customized checkout or a hosted payment page for simplicity.

Configure Your Settings

Rigorous Testing

Go Live and Communicate

Monitor, Analyze, and Optimize

Online Payments: The Real Scorecard (Benefits vs. Risks)

Your Strategic Advantages (The Upside):

-

Global Scale from Day One

Your physical location becomes irrelevant. You can acquire and service customers on the other side of the world as easily as local ones and effortlessly collect online payments from them.

-

Automation That Cuts Costs & Errors

Manual billing, invoicing, and reconciliation are profit drains. Automating these processes reduces labor costs and eliminates expensive human mistakes.

-

Superior Security as a Standard

Modern gateways offer built-in, AI-powered fraud screening that’s lightyears ahead of manual card handling. This isn't just a feature – it's active risk reduction.

-

Data That Drives Decisions

Every transaction is a data point. You gain direct insight into customer buying habits, preferred payment methods, and lifetime value, enabling precise marketing and sales strategies.

-

Checkout as a Conversion Engine

A fast, optimized payment flow is a direct driver of customer satisfaction and repeat business. In a competitive market, your checkout experience is a core part of your brand promise.

The Inevitable Challenges & Your Game Plan (How to Win):

-

Fighting Fraud

Your Move: go beyond basics. Mandate CVV and Address Verification (AVS), and enforce 3D Secure for high-risk transactions. For businesses in targeted sectors, generic tools aren't enough. In such cases, working with a payment partner that supports advanced, customizable fraud rules can significantly reduce risk.

-

Managing Chargebacks

Your Move: chargebacks ($15-$25 per dispute) erode revenue. Combat them with unambiguous billing descriptors, exceptional pre-dispute customer service, and irrefutable proof of delivery. A provider with dedicated dispute management support transforms this from a cost center into a controlled process.

-

Ensuring Uptime

Your Move: when payments go down, sales go to zero. Demand a provider with a contractual >99.9% uptime guarantee and always maintain a backup payment option. Reliability cannot be a compromise.

-

Navigating Compliance

Your Move: PCI DSS is non-negotiable. Simplify compliance dramatically by using a PCI-validated (SAQ A) gateway that assumes the burden. A true partner doesn't just offer compliance; they guide you through it and keep you aligned with evolving regulations like GDPR/CCPA.

Future Moves: What’s Next For Online Payments (2026-2030)

-

AI and Machine Learning Supremacy

AI will no longer be limited to fraud prevention and will become a driving force on enabling hyper-personalized checkout experiences, serving the best payment method for each unique user in real time according to likelihood of conversion.

-

The Emergence of Central Bank Digital Currencies (CBDCs)

Government issued digital fiat coins are being experimented on across the globe. Commerce must get ready for the possibility of CBDCs being used as a new, super-secure payment rail.

-

Frictionless “Invisible” Payments

Payments will disappear into the background. Think Uber – though with the payment happening automatically some time after the ride is over. This will spread out to retail through sensor fusion and biometric authentication.

-

Voice Commerce Growth

with increased accuracy in smart speakers voice-activated ordering for replacement items will take hold and backend systems that can automatically accept electronic payments through voice will be needed.

-

Super-App Payments

In the West, companies such as PayPal and Shopify are becoming super-apps that offer a range of commerce, social and financial services in one app to make payments more convenient (i.e. centralized).

Your Strategic Payment Partner for Complex Growth

BillBlend is more than a payment gateway – it’s your partner for:

-

Custom Solutions for Specific Verticals

Specialized knowledge and technology developed to service your sector with its distinct requirements and industry-specific regulatory standards.

-

Solid High-Risk & Global Payment Management

Ensured payment take-up and fit with wide range of cross-border settlements where others fall short.

-

Deep Integration & Automation

Sophisticated, customizable APIs and automation tools that seamlessly connect payments with your own operations stack.

-

Proactive Security & Compliance Leadership

Proactively address fraud, risk, and regulatory compliance (PCI DSS, GDPR, CCPA) rather than react to issues in the midst of process.